In any economic environment it is of critical importance to manage the expenditures of the Organization. In this current period where continuing to grow revenue levels may be difficult for a business, cost cutting options are often explored. Whether as a result of a survival instinct or standard business practice, the basic goal of the organization is to continually reduce the costs of the business, as minimally required to produce revenue in the attempt to increase the overall net income.

Cost cutting : Reduce costs to produce revenue – goal: increase net income

Service companies differ from Product companies in that typically the cost of Labor is the most significant. For Product companies it is often the Cost of materials for resale.

Spend management is the way in which companies control and optimize the money they spend. It involves cutting operating and other costs associated with doing business. These costs typically show up as "operating costs" or SG&A (Selling, General and Administrative) costs, but can also be found in other areas and in other members of the supply chain.

An organization has two discrete “buckets” to consider; revenue and cost. Costs are incurred by a Company during the course of business – selling something. Of the costs there are fixed and variable costs.

In hard economic times, when revenue is harder to come by, companies often turn to cost cutting initiatives. Cost cutting will increase net income. An increase in net income leads to a greater earnings per share and ultimately a higher market value (higher market capitalization).

Companies typically turn to the easiest cost cutting measures. This can be expressed with layoffs and product quality reductions due to material changes. However, most analysts agree that this short term tactic creates little long term value, nor any long term sustainable savings. This is why "Spend Management" has become a key long term strategy for companies seeking to maintain long term and sustainable value.

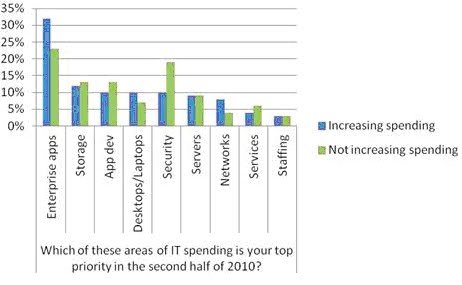

2010 Spending Priorities (SearchCIO.com, April 2010) mschlack@techtarget.com | |

Companies typically turn to the easiest cost cutting measures. This can be expressed with layoffs and product quality reductions due to material changes. However, most analysts agree that this short term tactic creates little long term value, nor any long term sustainable savings. This is why "Spend Management" has become a key long term strategy for companies seeking to maintain long term and sustainable value. |  |

Spend Management is a subset of Total Cost Management

Spend management as a subset of total cost management falls into a category described as the ePurchasing market. This is predominately due to the nature of software available used to analyze spending patterns. Forrester Research estimates that this market as a total of software solutions is expected to grow at rate over 3 percent for the coming year, $3.5 billion in 2009. This advanced software licensing is affected by the modest growth in the global recession and weak credit market conditions. The Forrester Reasearch work also identifies market leaders Emptoris and Ariba, while Oracle and SAP enterprise vendors encroach on the smaller players by making efforts in this market.

Tools Segment | |

Ariba | Oracle |

Emptoris | MethodR – Profiler |

Hotsos – HAWCS | |

There are several primary benefits of spend analysis software. The software is often helpful in consolidating the view of information. The aggregated data can help the organization identify areas of interest regarding increase of cost controls.

Example Benefits:

• Aggregate buys to get best volume discounts;

• Efficiently handle multiple suppliers;

• Provide information and analysis to negotiate better deals;

• Reduce the associated paperwork and processing;

• Achieve accurate insight into spending patterns.

• Efficiently handle multiple suppliers;

• Provide information and analysis to negotiate better deals;

• Reduce the associated paperwork and processing;

• Achieve accurate insight into spending patterns.

Source-to-Settle spending analysis

Procurement - Aggregate purchasing to get Volume discounts

Receiving - Efficiently handle multiple suppliers

Payment Settlement/Invoicing - insight into spending patterns.

Directly within the IT realm, Costs are often captured as the Total Cost of Ownership for the organization. This includes all the costs related to Software and Hardware acquisition and maintenance in addition to the Support Staff salaries.

In this time of Global business distress it could not be more critical to manage the Expenditures that describe the Costs. When considering the best way to reduce costs the organization must consider more than the “line items” on the Budget.

The overall Company budget will include items such as mortgage or rent payments for facilities as well as insurance, interest, taxes, utilities service and facilities maintenance. Other items such as cost of goods sold expenses, equipment, payroll expenses, raw materials may be split among the individual business unit cost structures involved.

Within the structure of a business there are many areas subject to Cost Management. Standard considerations to reduces costs may range from a distinct reduction in force option to a shared reduced compensation across a subset of the employees.

Travel expenses are an appropriate general indicator of business activity. Increased travel means the company is out, getting more customers. Historically, travel has been under formal management. Scrutiny has been given to the review compliance process to address corporate abuse. Recent scandals and compliance requirements make this expense category a good target. The management can be articulated differently between companies. A consolidation of travel policies across business units is a good beginning. In addition to category limits and per diem approaches to expense control. Review of the paperwork processing requirements often allows for significant cost savings by process re-definition. Some form of on-line automation of manual processes is typically the avenue of greatest improvement..

Often times the automation improvements applied to the travel re-imbursement process can be expanded to address more payment area issues.

Define Case Study of Manual Expense Flow vs. Oracle/SAP T&E flow (interfaces, re-key, etc.)

Source-to-settle (spend analysis, sourcing, procurement, receiving, payment settlement and management of accounts payable and general ledger accounts )

Other options like WorkFromHome may allow for a reduction in facilities requirements. A progressive alternative of offering a work-from-home option may be able to treated as exchange compensation for a reduction in salary. Many studies have shown that employees would often accept an opportunity to work by tele-commute instead of a direct compensation increase. In addition to the advantages to the employee to work from home is the broader environmental impact of reduced gasoline usage and exhaust from vehicles that are no longer commuting to work each day. If this strategy were expanded to include a larger percentage of the workforce the impact would be even larger.

In a similar fashion, the continuance of this strategy would setup hoteling work-stations. This continues to allow for trans-location employees to be productive when on-site.

(Expand to include environmental repercussions)

As part of an Organizations Disaster Recovery plan, it is reasonably appropriate that the IT organization be prepared and capable of supporting the business’ requirements even if facilities are compromised in some fashion. When defining the Business requirements for disaster support certainly the Organization may have to be able to support anywhere from 30-70% of the work force. This requirement could last for an uncertain amount of time.

In some cases the IT Group does not have direct control over Salary budget items regarding direct-control and cost reduction options. Often this budgetary responsibility is predominately in another area of the Organization.

In order to yield the greatest impact from any cost reductions the level of contribution of that element must be considered.

THIS IS THE SAME METHOD USED FOR PROFILE TUNING

The computing costs of the IT organization are described as separate elements, hardware, software, salaries. These areas contribute an estimated 68% to overall costs. In order to properly measure costs the volume of activity or workload must also be considered. In general it is easy to understand that the more activity we can accomplish within the constraints of our computing capabilities without increasing direct costs the better. This means we must make things go faster.

The cost savings implications can be significant. When we consider that the simplest of performance reviews begins with considering the total volume of pre-scheduled, thereby predictable, tasks.

By review and identification of these tasks, the most critical task to the business may be identified. Determining the criticality can be tricky. For example, it is easy to recognize that the speed with which Orders are able to be entered is directly related to Sales. Increase the Order intake speed and revenue increases. Likewise, although maybe not as identifiable something like Invoicing may seem non-critical, however delaying the recognition of revenue is equally critical.

It is difficult to describe the situation simply . . . We cannot just consider a fixed workload volume, 10,000 transactions, requiring an hour to process. This information alone would yield a cost of over $34 per transaction using a $300,000 annual TCO. In order to use this method with such a limited task set we would need to be able to identify this tasks percentage as a statement of total computing requirements. If we were able to say the Order interface was 1% of our computing requirement this would reduce the costs to a vaguely more reasonable $.30 per transaction. Still quite high and incorrect.

My work in performance tuning from profile analysis has yielded great results. Typically my work can be described by a 10:1 ratio of “savings” vs. costs. Most engagements recognize from 45-95% improvements in Response Time yielding 100s of thousands of dollars in capacity utilization savings minimally allowing other tasks to execute with the recovered capacity.

Continuous process improvement and performance tuning requires continuous measurement and tracking

· Define

· Measure

· Analyze

· Improve

· Control

Improvement begins with defining the critical business tasks to be considered.

After identified, the current performance of the target task must be properly measured, as a base-line.

The measurement results are reviewed and analyzed for opportunities for improvement.

Establish the recommended changes to address performance findings.

Re-test and re-measure the performance after the recommendations are implemented. Implement as appropriate or return to step 2.

Conclusions

Enough is enough. Corporate leaders are properly raising the bar of expectation: the IT core mission should be expanded from mere cost-cutting to enable revenue generation within a short period of time. A significant question to sole is the HOW of encouraging such innovative behavior.

. . .

When making decisions – caution is advisable.

First, freeze. Stop and review your schedule spending activities.

Stop hiring activities – regardless.

Remove discretionary spending approval from everyone.

Firing people – although a direct cut – lay-offs have multiple secondary effects, including the reduction of morale and motivation by the remaining staff. Unless the RIF is an opportunity to rid yourself of a “bad egg”, it’s probably better to make a shared cut in compensation of all staff. Certainly a person facing a RIF might likely accept a reduced salary – versus a 100% pay cut.

Be creative – sure there are management skills required, but creativity doesn’t come with an MBA. Ideas are the true life-blood of a company.

Energy – there are a number of simple options. For example, unless your electricity is paid by the Landlord, put a common timer on the refrigerator in the Common Area. Set it to only run from 6am to 6pm. This will reduce the appliance consumption by 50%.

Parking lot lights are also an area where a small investment in motion detectors would reduce the use substantially. Add one or more motion sensors to each light pole in the parking lot, such that the lights only come on at night when there is motion. Four sensor will allow coverage for most areas. The sensors should be placed 10’-15’ above the ground. This motion detection helps alleviate most security concerns. This could reduce the related energy consumption over 80% depending on the traffic in the area.

. . . to be continued

Reference:

Forrester Research : Predictions 2009: ePurchasing Market, ./Research/Document/Excerpt/0,7211,44129,00

Spend Analysis: The Window into Strategic Sourcing, Pandit, Kirit; Marmanis, H. (2008), ISBN 1-932159-93-6

2010 Spending Priorities, SearchCIO.com, April 2010, Mark Schlack, Editorial mschlack@techtarget.com

0 comments:

Post a Comment